Cutting bills and creating jobs

The economic opportunities of a clean energy transition

Science makes clear that to stabilize the climate, we must rapidly phase out fossil fuels and replace them with a clean energy system. Governments hold the key to making this happen. What often holds them back is uncertainty about what this means for the people and the economy of their country.

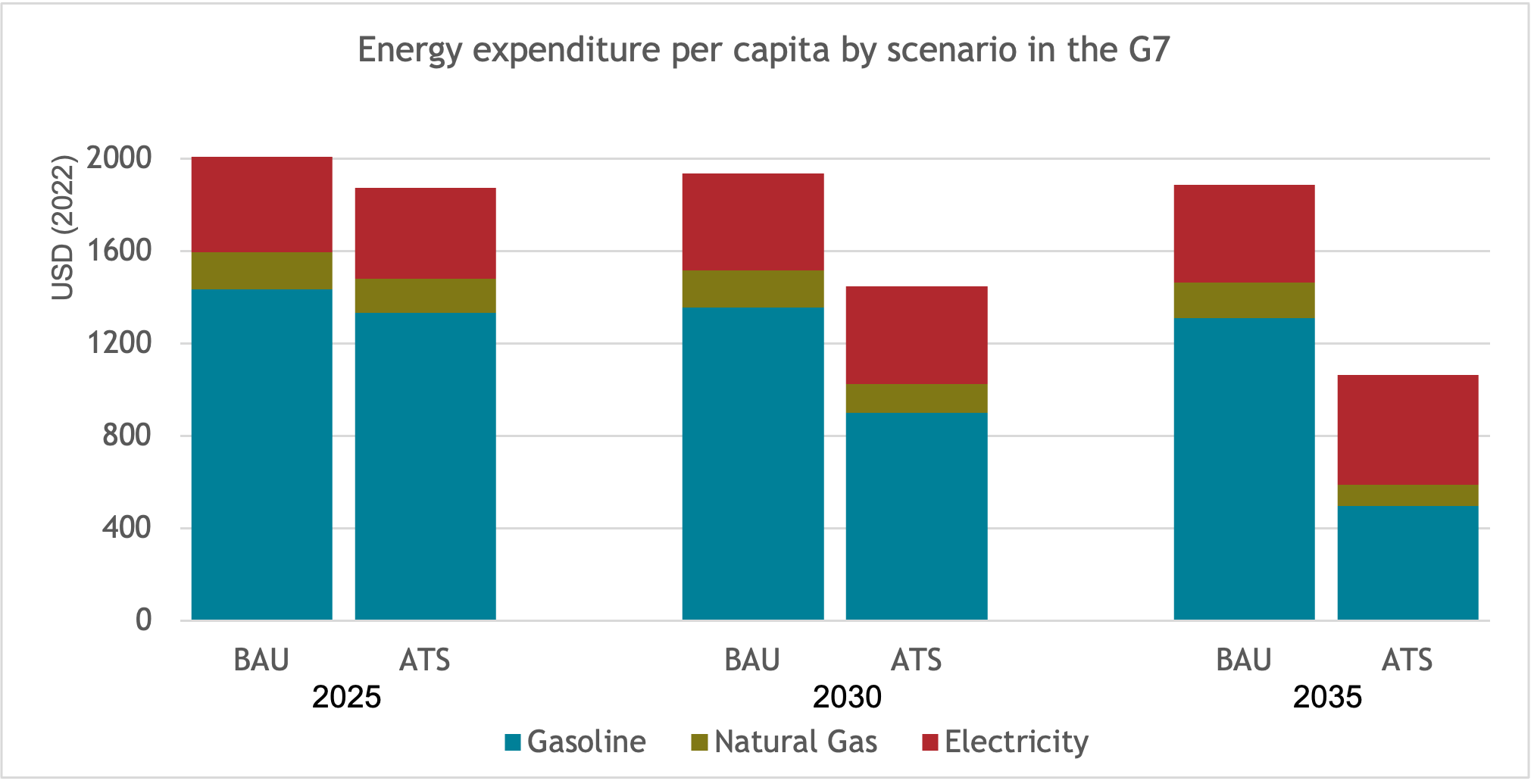

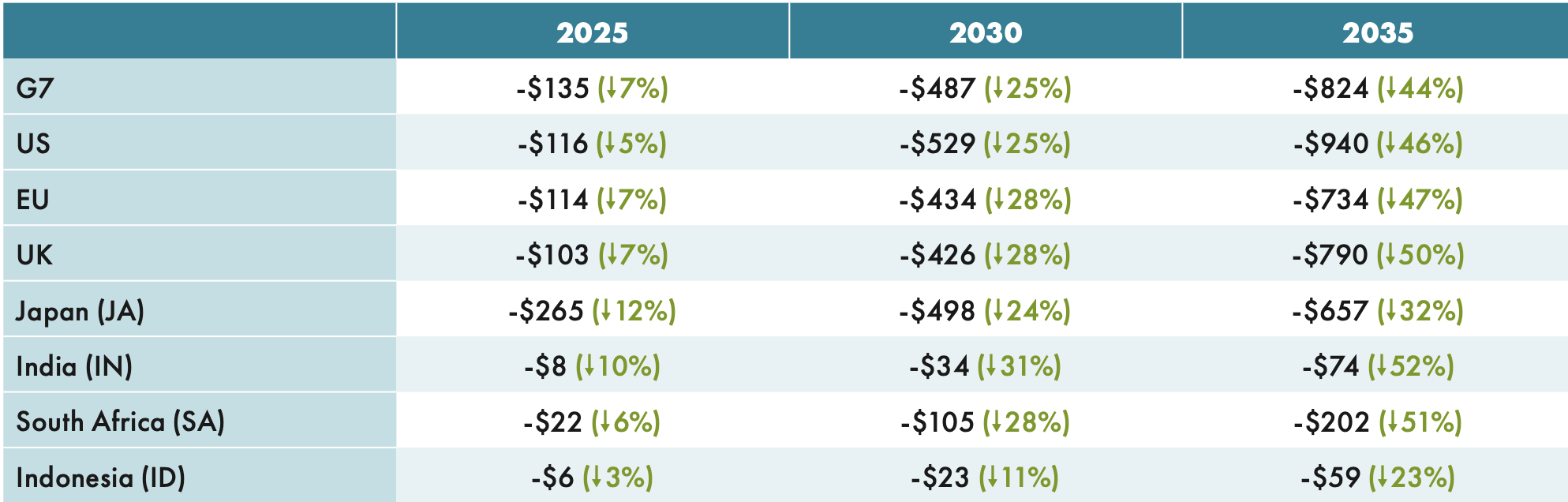

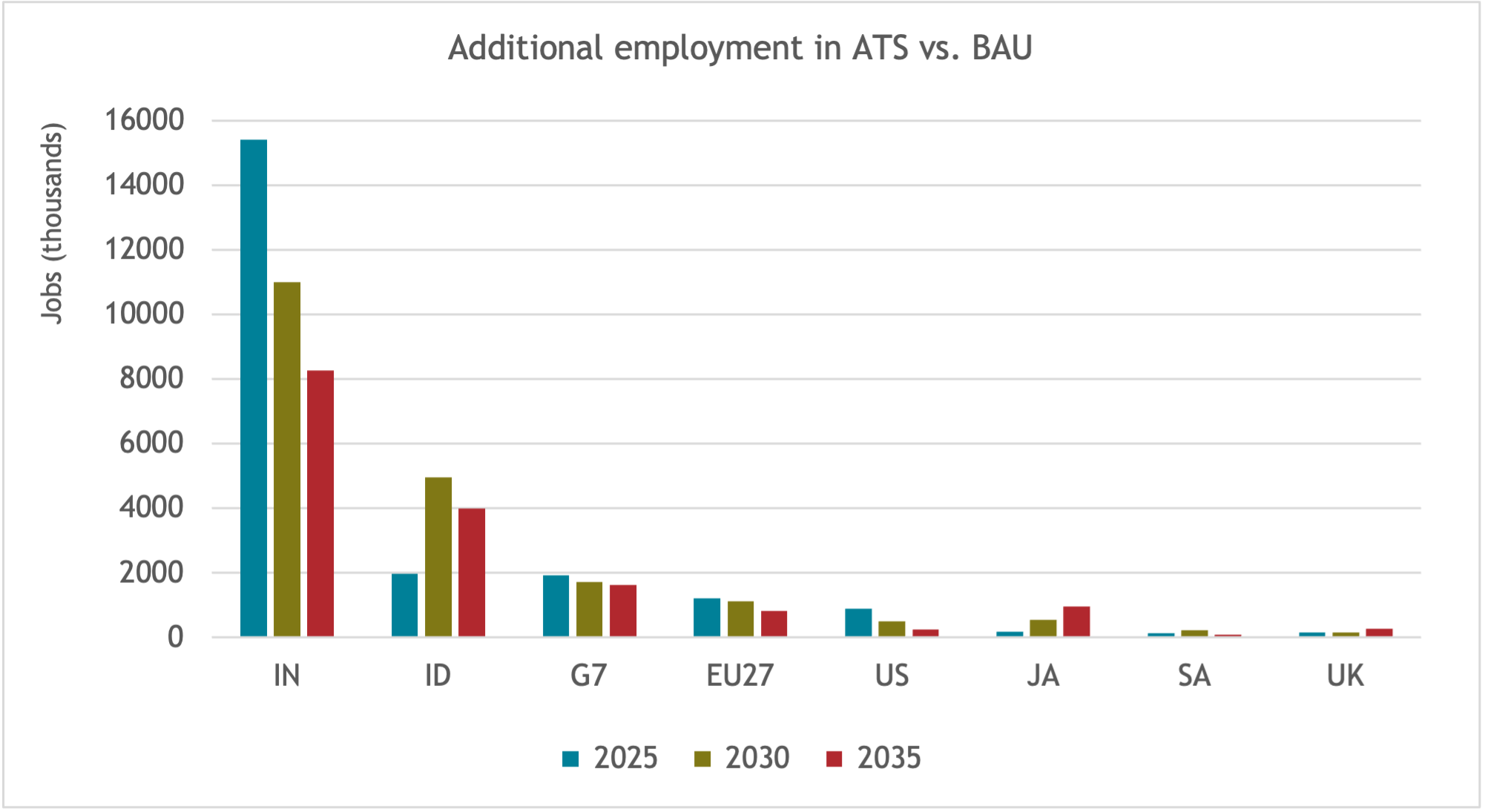

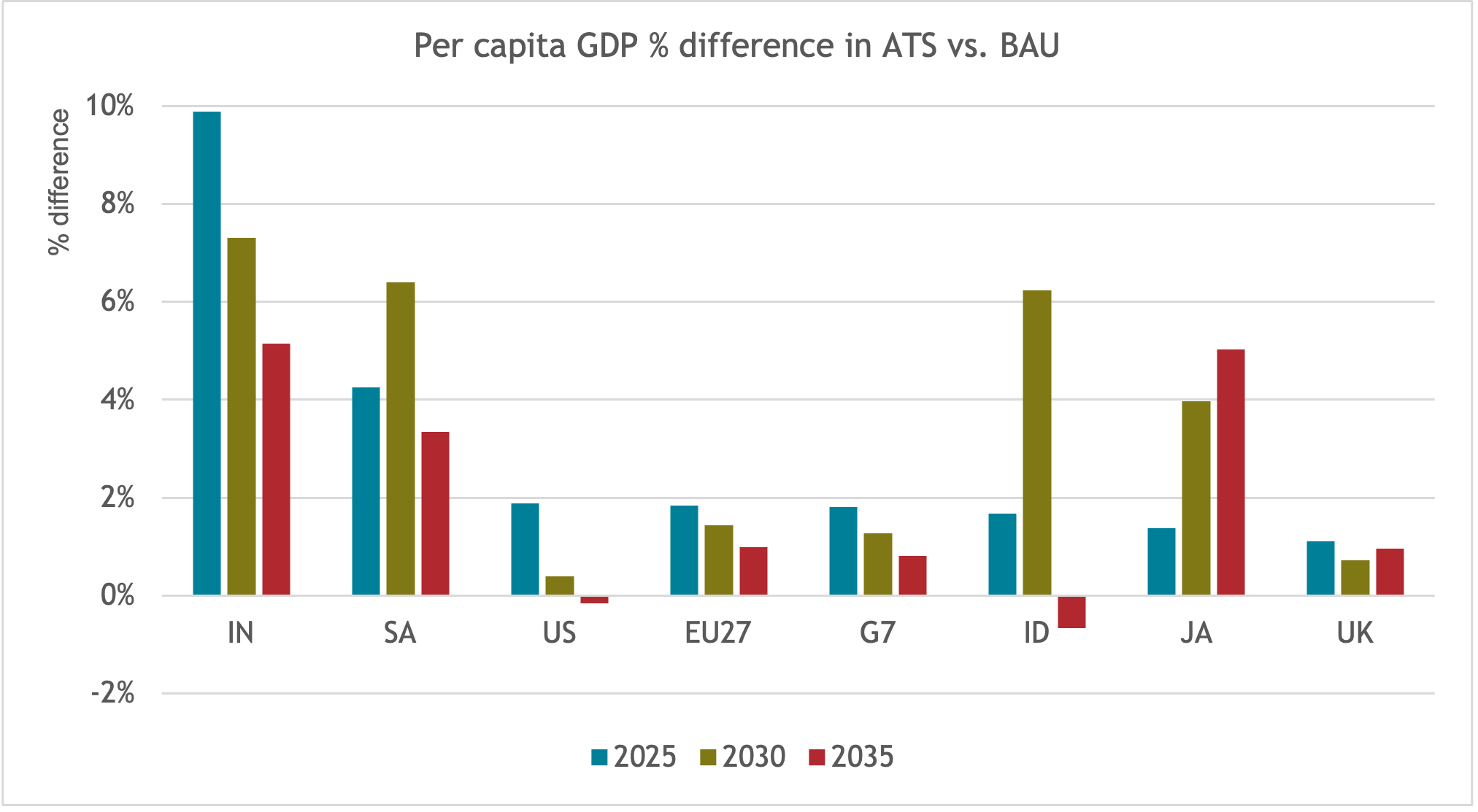

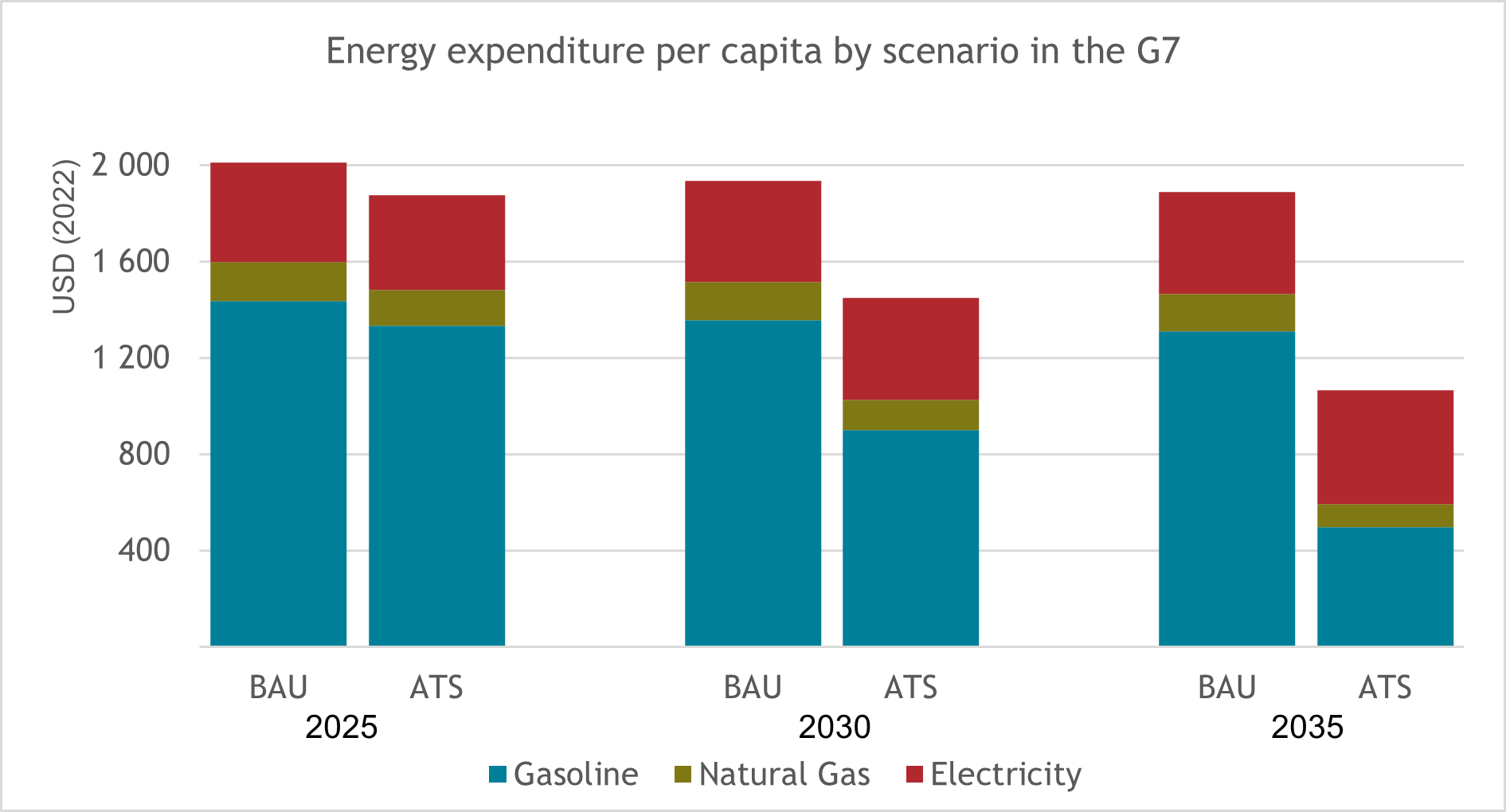

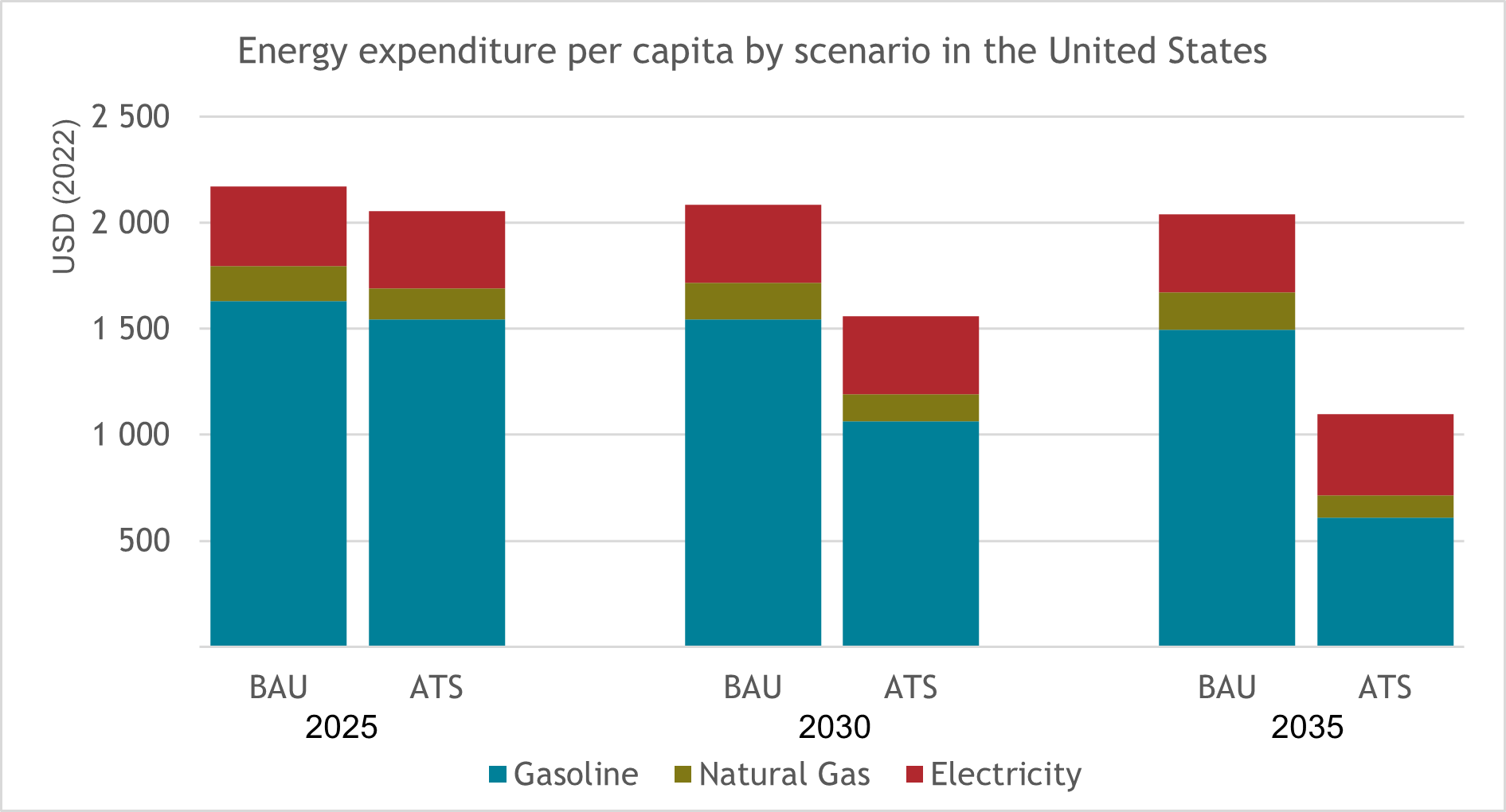

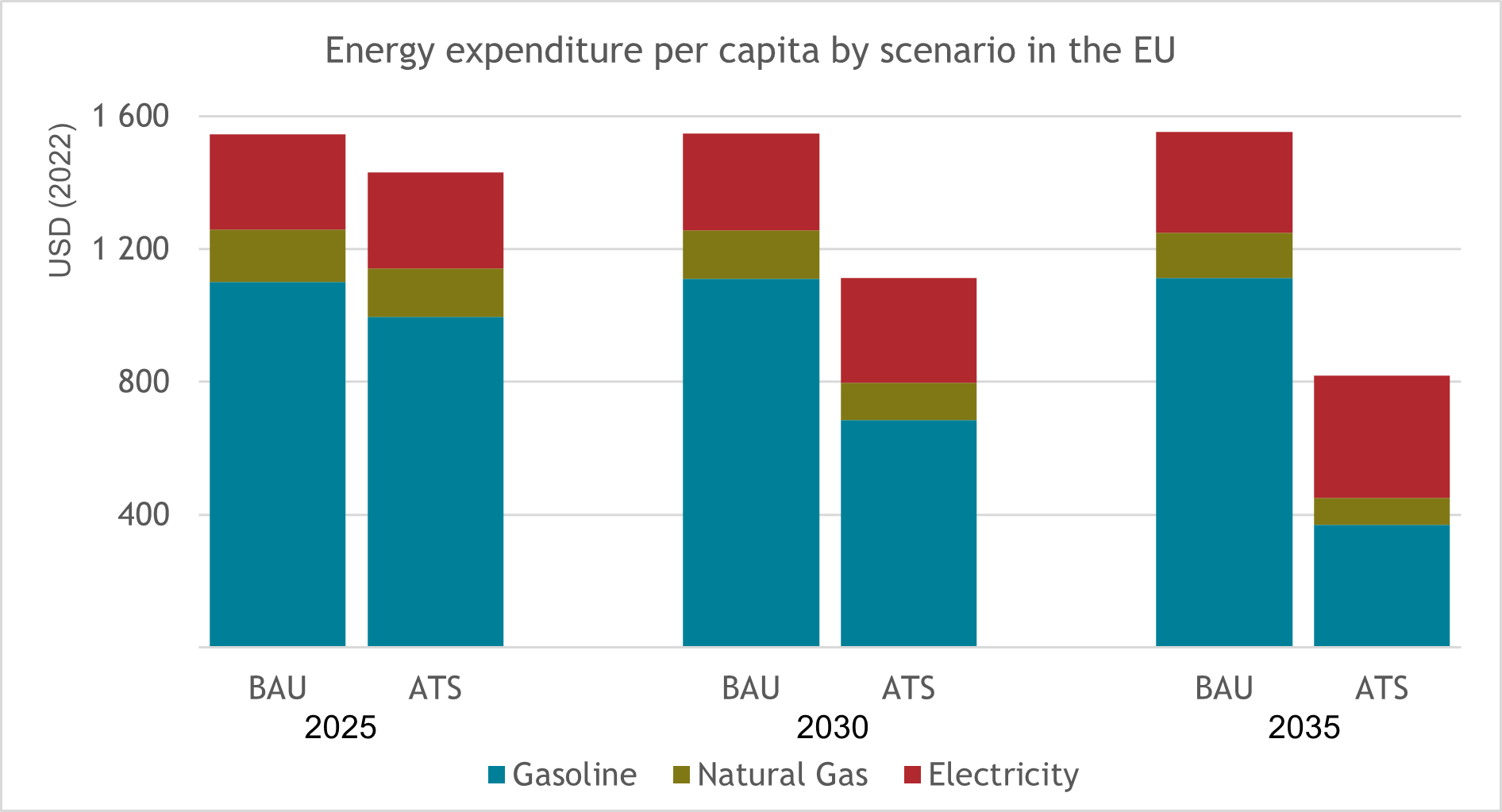

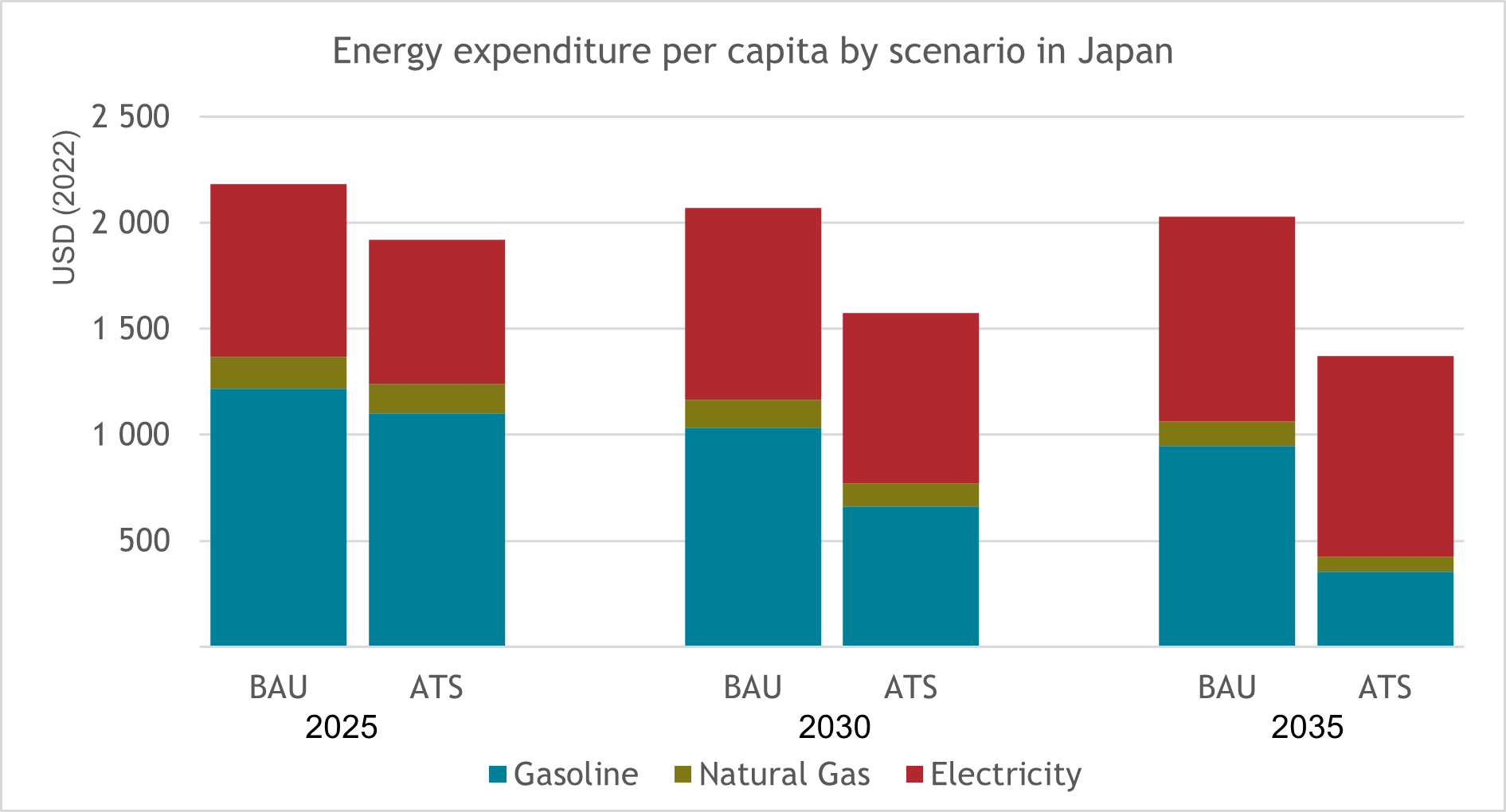

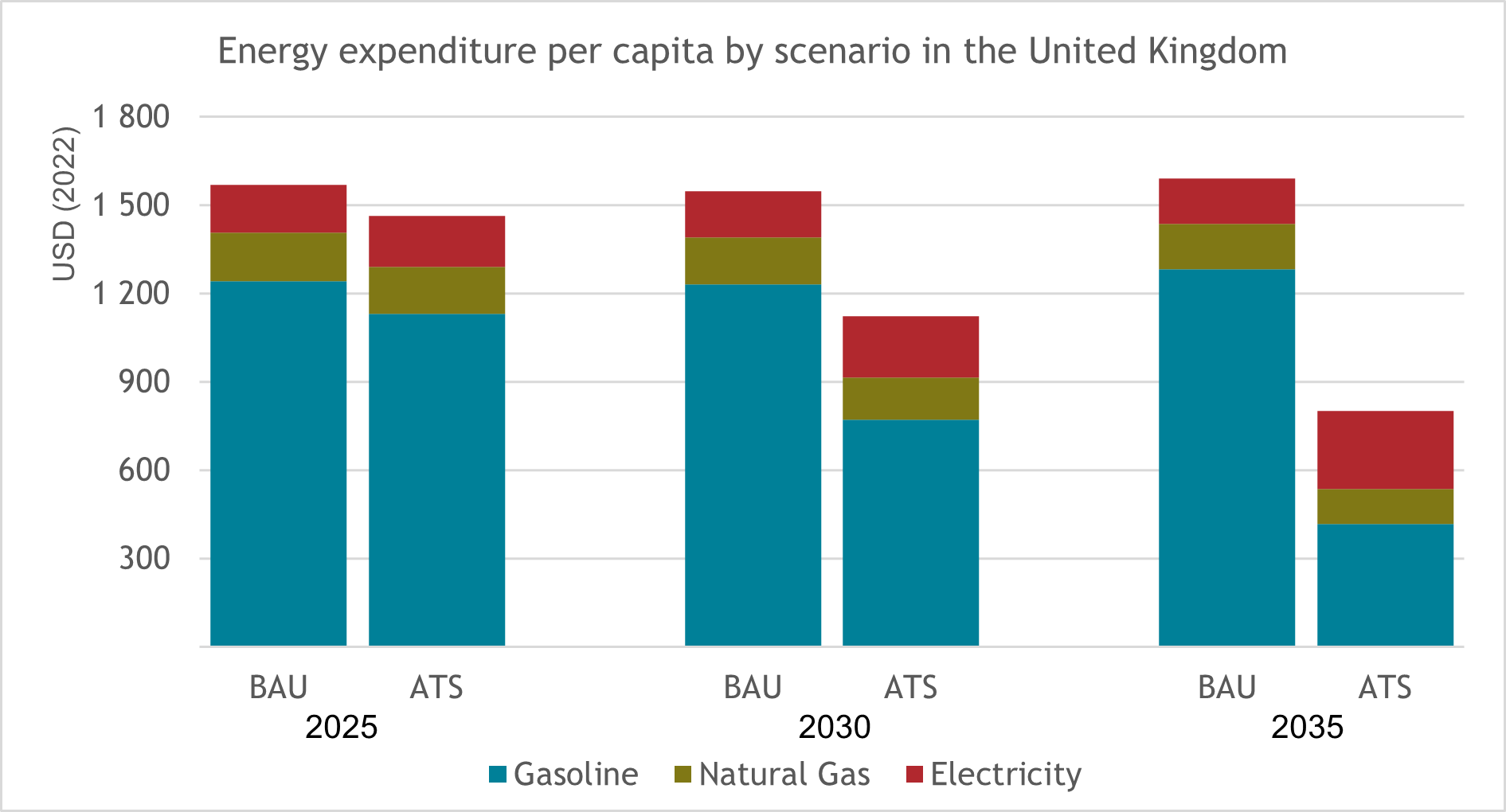

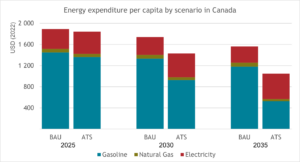

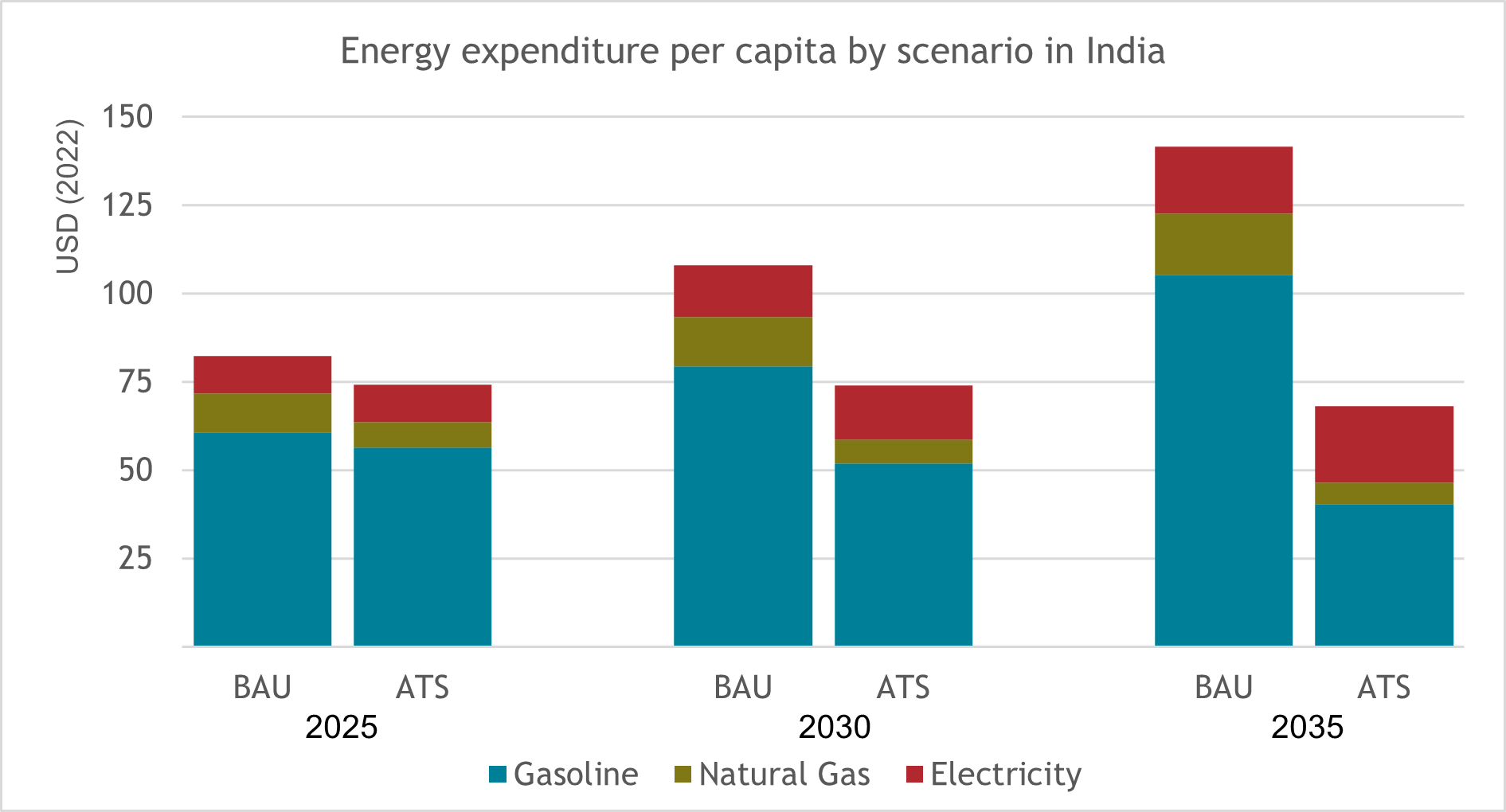

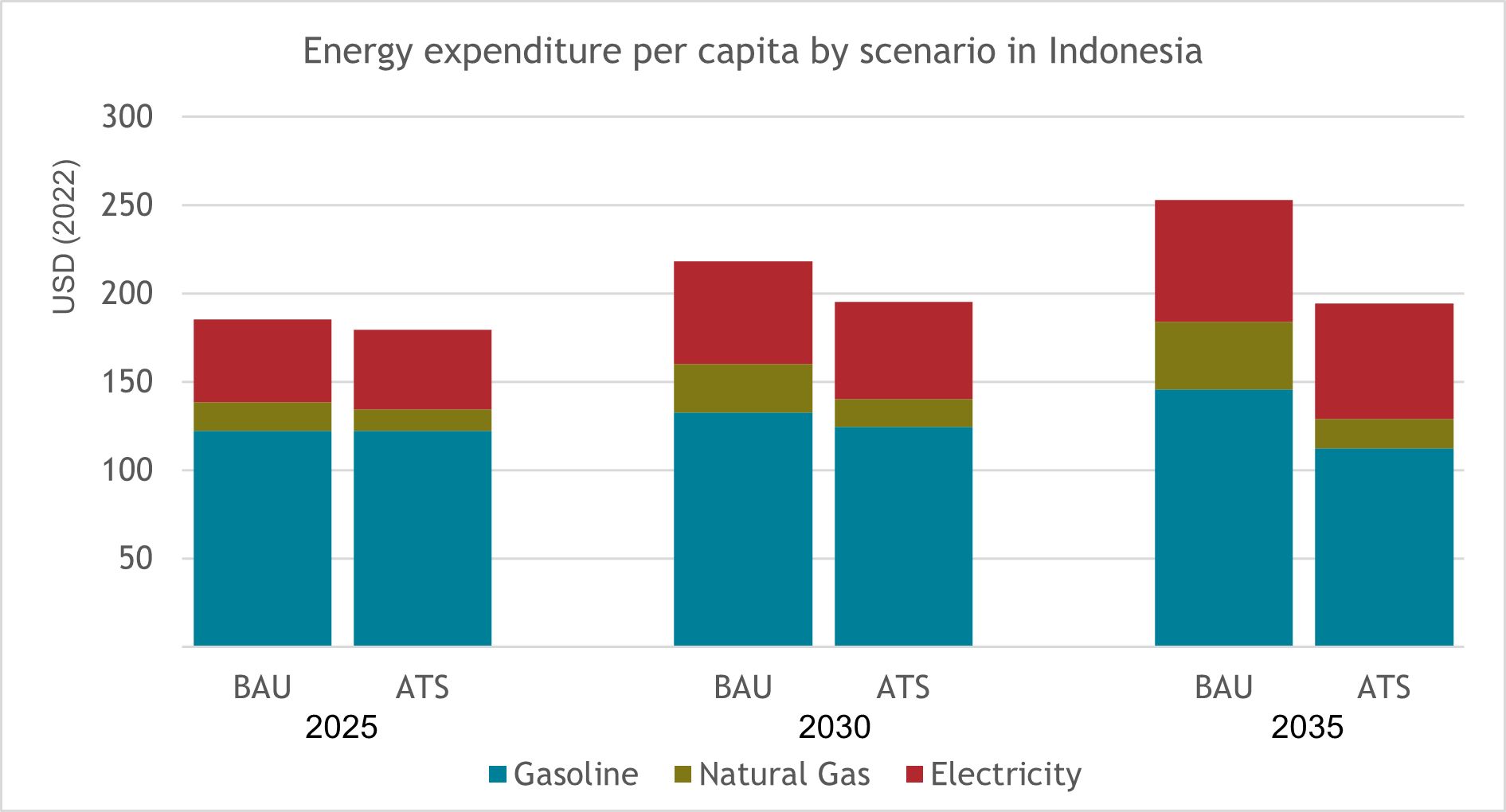

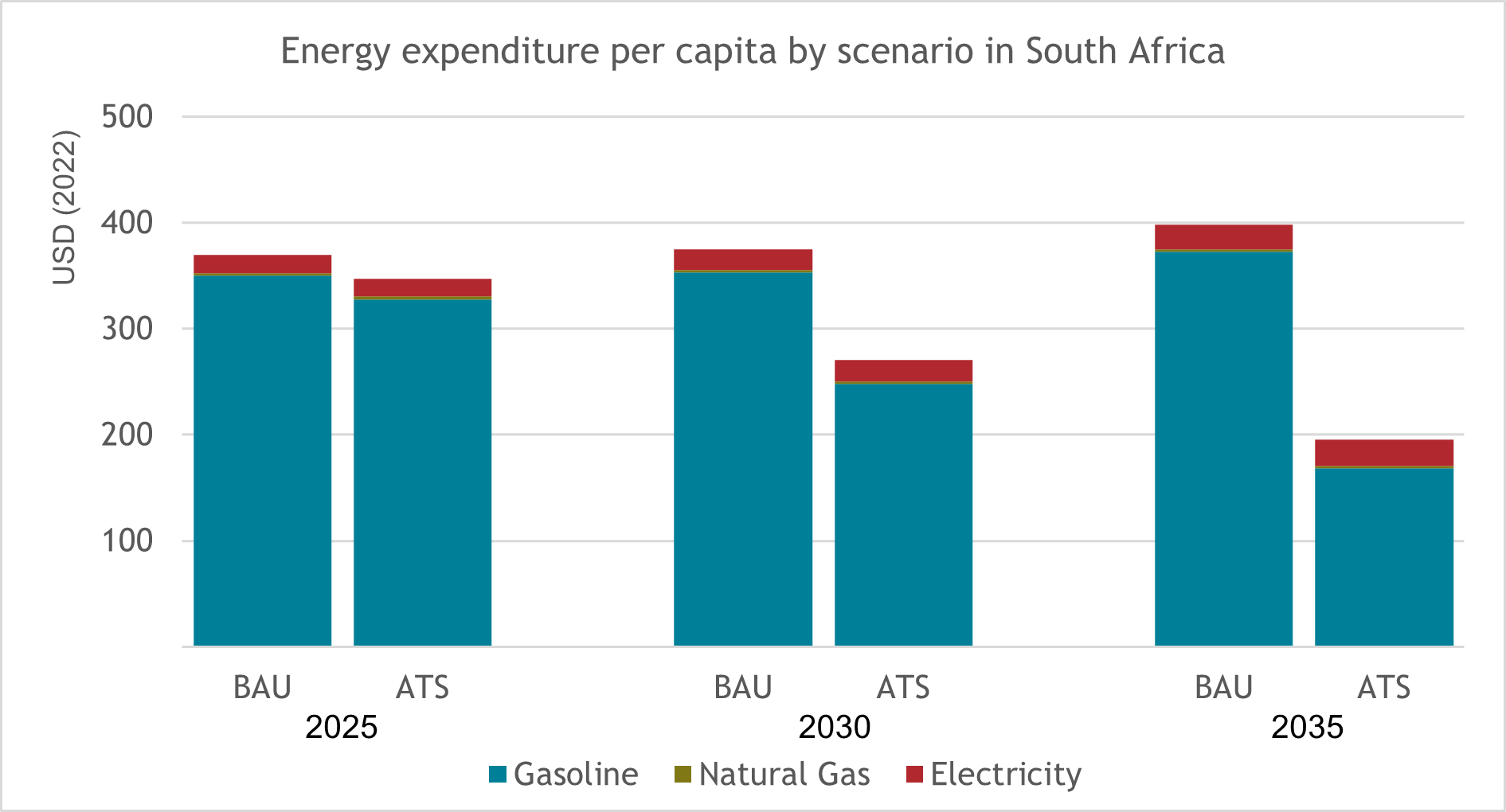

Our new socio-economic analysis and modelling, commissioned from Cambridge Econometrics, shows that the clean energy transition is affordable and in our economic best interest. The research finds that government policies that accelerate the cleaner energy transition to net zero will reduce future energy bills and create jobs while maintaining GDP growth in both advanced and developing economies.

- Download: Summary for policymakers (pdf, 859KB)

- Download: Full report and modelling (pdf, 4.8MB)

Policies backed by forward-looking businesses

Over 1,000 companies headquartered in nearly 60 countries, have joined calls for governments to set policies that accelerate the transition to clean energy and keep 1.5ºC within reach. They have put their name on public statements to the G20, European Union, United States, Japan, and United Kingdom.

Businesses are calling for governments to deliver specific policies that will help accelerate the transition of the global economy to net zero emissions mid-century.

The We Mean Business Coalition commissioned Cambridge Econometrics to model a business-as-usual scenario vs an accelerated transition scenario where governments have delivered policies to accelerate the transition away from fossil fuels to net-zero.